Curious about whether your current withholdings will be sufficient under the new tax laws? The IRS has made available a new self-service online tool which can help you determine this. It is important to read the instructions carefully before you start, as you will need to have documentation handy to answer several of the questions (e.g.most recent tax return, pay stubs).

The system will prompt you for missing information, but you will need to know things like your projected income for 2018, and number of children who qualify for the child tax credit (they must be under age 17 as of 12/31/18), so make sure to gather everything you need before you start the questionnaire. Also, please note that If your health care is through the Health Connector, this amount will not factor in to the ACA premium tax credits.

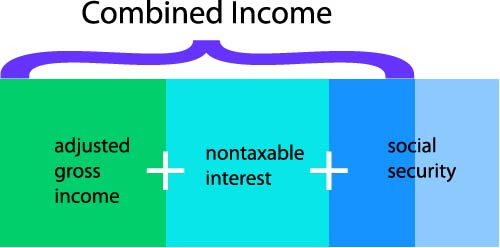

According to the IRS, the formula to determine if you will pay taxes on your Social Security income is to take one half of your Social Security benefits and add that amount to all your other income, including tax-exempt interest. This number is known as your combined income (combined income = adjusted gross income + nontaxable interest + half of your Social Security benefits).

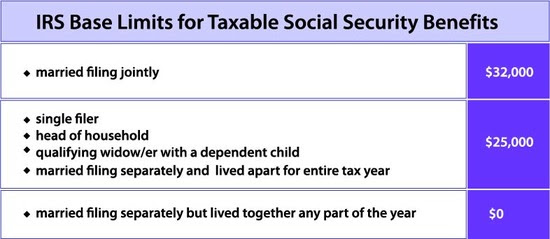

If your combined income is above a certain limit (the IRS calls this limit the base amount), you will need to pay at least some tax. The limit is $25,000 if you are a single filer, head of household or qualifying widow or widower with a dependent child. The same applies if you are married filing separately and you lived apart from your spouse for the entire tax year. The limit for joint filers is $32,000. If you are married filing jointly and you lived with your spouse for any part of the tax year, all of your Social Security income is taxable.

When retirees need extra money their first choice is generally taking an additional IRA distribution. What they may not realize is that this is taxable income, and therefore it increases their taxable Social Security amount. For example, an additional $12,000 IRA distribution may increase the taxable Social Security portion by as much as $6,000.

If it’s available to you, the safest bet for an immediate cash need is to use your savings. Though this may seem counterintuitive, you can see how adding any money that is considered taxable income to your base limit could potentially end up costing you money.

For the same reason, if you do need to take an additional distribution from your IRA, make sure you think about how much you really need. For instance, if you only need $5,000, but take $10,000 with the idea that it will give you a rainy day fund, at least some of that money may be eaten up in taxes if it causes your taxable income to exceed the base limit.

Whatever your circumstance, we are here to help. Give us a call if you have questions about the best course of action for your particular situation.

Last fall we gave you a heads up on one of the significant impacts of the Tax Cuts and Jobs Act for 2017: the loss of itemized miscellaneous deductions for employees. The IRS issues Publication 529 as a guide outlining what is deductible—and what’s not—under current tax regulations.

We like to remind our clients that tax laws are always subject to change. And likewise, personal situations may change during the course of the year that will affect your returns the following April. For instance, perhaps you started a new job this year that requires you to pay union dues, or work from home. Except for a very few specific categories of employment, employee deductions for everything from uniforms to meals and mileage has been disallowed. Be sure to check with your employer to see which, if any, out-of-pocket expenses you can expect reimbursement for before you make any purchases related to your job. And either way, remember to keep your receipts!

In the meantime, here is a link to the IRS website with current information about Publication 529.

Late last fall, we predicted that changes from the Tax Cuts and Jobs Act of 2017 would have a significant impact on many of our clients in 2018. Unfortunately, for most of you that impact came in the form of refunds that were $3,500 to $4,500 lower, or balances due that saw an increase of $5,000 to $7,000 over the previous year.

How did this happen? What we found is that the withholding tables under the new tax code are severely skewed—in the wrong direction for many taxpayers. In order to correct the situation for our clients who would like to see their refunds or amounts owed come closer to 2017 levels, we are suggesting a simple solution: Adjust your withholding now.

To make this adjustment you’ll need to complete a new W-4 form,and fill in the extra amount you want withheld on Line 6. Just be sure not to change your filing status (e.g. if you currently claim “Married -0-“, do not change that).

For example: Say you saw a $4,000 difference between 2017 and 2018, and you have 10 pay periods left this year. Simply divide the amount by the number of pay periods and add the result to the withholding amount for your remaining paychecks. In this case, $4,000 ÷ 10 = $400 per paycheck, so you would enter $400 on Line 6 of your new W-4.

The problem is also magnified if you have multiple sources of income. A married couple that has three or four W-2 forms will see a lower federal withholding on their second job(s), which may not cover what is owed.

Consider this: Most people earning between $25,000 and $50,000 will only have 7% or 8% Federal tax withheld from their paycheck. Since many taxpayers in this situation may have income from other sources that put them in the 22-24% tax bracket, the minimal 7% or 8% federal withholding will likely result in a balance due.

You’ll need to remember that increasing your withholding will reduce the amount of your paychecks, but if your income is similar to 2018 you’ll see a corresponding increase in your refund, or decrease in your balance due, for 2019.

Feel free to contact our office if you have questions, or need help determining whether and how much to adjust! [email protected] or 781-337-8788

Meeting with clients about their taxes as we approach year end—or worse, during the height of filing season—is almost like trying to plan your vacation on your flight home. Traditionally, clients most often come in to meet with us during February and March, which limits our discussion to a prior year’s tax filing. And because the main focus is to complete your income tax return at that time, we are constrained to discussing only past events.

1. They both require planning.

You’ve probably never thought about it quite this way, but just like a vacation, maximizing the tax benefits you are entitled to requires some advance planning.

2. The best months to plan are May, June, and July.

Although it may seem counter-intuitive at first, removing the pressures and deadlines of tax filing season translates to more focused, big picture planning.

Over the course of the last three years we have determined that the best window for effective client meetings is from late spring through early summer. This timeframe allows us to take a longer view of your financial future and provide more in-depth assistance that will be to your advantage.

Whether you are interested in seeing us for current tax planning, budgeting assistance, or exit strategies for retirement, we are confident that—just like a good vacation—scheduling these meetings in warmer weather will take away some of the stress of tax planning and bring the most benefit to all of our clients. Keep an eye out for more information about scheduling financial strategy meetings with us in 2019.

Unfortunately, we continue to hear frequently from clients who are concerned about threatening phone calls claiming to be from the IRS about delinquent taxes. Please know that the IRS will never initiate contact with you via email, nor call and threaten you with arrest. We cannot state strongly enough that you should never send personal financial data in response to an unsolicited email, nor give it over the phone to someone you can’t verify.

Criminals continue to find new ways to steal people’s money and identities. One of the latest scams involves trying to direct you to a phony IRS website that will ask for personal data. The following link will take you to the real IRS website for information about the many phone and e-mail scams that are currently making the rounds: https://www.irs.gov/newsroom/tax-scamsconsumer-alerts

We also want to make you aware of a new payroll theft scheme where employee login information is stolen through fake e-mails. Once cybercriminals have this, direct deposits can be diverted to fraudulent accounts. The link below is a public service announcement from the FBI detailing the specifics. https://www.ic3.gov/media/2018/180918.aspx

Before you upload your documents to the portal this tax season, take a moment to make sure you have collected everything we’re going to need to process your return. We keep a log of client upload notifications, and process them in the order they are received, provided that we have all of the necessary documentation. If information is missing and/or if we receive multiple notifications of uploads to your folder, you will be required to notify us when the FINAL upload has been submitted. This will allow us to log you in as received and begin processing your returns.

One upload per client ensures that we can keep returns moving through as quickly and efficiently as possible. Thank you for helping us continue our commitment to excellence in customer service!

The Mass Health Connector will send Form 1095-A to members by the end of January. Those insured through the Health Connector should wait to get a Form 1095-A before filing their federal tax return.

If you had a 2018 ConnectorCare plan, or a monthly tax credit to lower your premiums in 2018, you must file a federal income tax return.Filing is a requirement even if you normally don’t file a federal tax return because you have no income or your income is low.

What is Form 1095-A?

Form 1095-A provides the following information for Health Connector members

Months covered by the Health Connector

How much tax credit was applied to monthly premiums in 2018

Unfortunately, we continue to hear frequently from clients who are concerned about threatening phone calls claiming to be from the IRS about delinquent taxes. Please know that the IRS will never initiate contact with you via email, nor call and threaten you with arrest. We cannot state strongly enough that you should never send personal financial data in response to an unsolicited email, nor give it over the phone to someone you can’t verify.

Unfortunately, we continue to hear frequently from clients who are concerned about threatening phone calls claiming to be from the IRS about delinquent taxes. Please know that the IRS will never initiate contact with you via email, nor call and threaten you with arrest. We cannot state strongly enough that you should never send personal financial data in response to an unsolicited email, nor give it over the phone to someone you can’t verify.